Catalyzing Tomorrow’s Chips: Semiconductor Trends and RF Technologies in Semiconductor Equipment

ICAPS Semiconductor market Trends and RF Technologies are reshaping the landscape of chip design and manufacturing across key ICAPS markets – IoT, Communications, Automotive, Power & Sensors.

On a global scale, as electric vehicles and semiconductor-capable devices connect, the physics of RF-intensive architectures (tens-of-gigahertz bandwidths), wide-bandgap materials, and advanced plasma-based fabrication processes must underpin changes in semiconductor equipment. Those semiconductor trends and RF technologies impact RF circuit integration, plasma-based etch processes and deposition tool architecture, thus making them the nerve center of the next phase of semiconductor manufacturing evolution.

Semiconductor Trends and RF Technologies in ICAPS Markets

The semiconductor industry is increasingly driven by ICAPS markets – IoT, Communications, Automotive, Power and Sensors rather than just traditional PCs or servers. The fast growth of connected devices and the adoption of electric vehicles (EVs) is driving demand for chips that integrate RF, power, and sensor functionality.

Analysts expected the number of connected IoT devices to grow nearly 30billion of by 2027[1], through automotive, industrial, smart-home, wearables and healthcare. Such applications require specific chips (low-power radios, high-frequency transceivers, mixed-signal ICs) at various nodes.

For instance, market research indicates IoT and automotive IC segments are growing at a >13% CAGR rate to reach >$20–28B in sales (2017 baseline). CMOS logic, BiCMOS, SiGe and even wide-bandgap (SiC/GaN) and piezoelectric materials have now become key technologies across legacy (>100nm) to advanced (<7nm) nodes[2].

Semiconductor Market Trends and RF Technologies in Semiconductor Fabrication Driving IoT, Automotive and Sensor Technologies

Demand for RF technologies in semiconductor fabrication, power and MEMS chips from a rapidly growing number of connected devices, EVs and sensors is forcing fabs to upgrade equipment, optimise processes, and maintain cleanroom standards.

1. IoT & Communications

Ultra-low-power mixed-signal chips are needed for massive networks of sensors and radios (BLE, Wi-Fi, 5G). Demand for RF front-end modules and transceivers[3] is driven by the connected-device count (~30B by 2027[1]) and growing 5G networks. This drives equipment upgrades for mid-tier nodes (e.g. enhancing 28–55 nm lines for RF) to boost yield and power efficiency.

Our Equipment Engineering services ensure your semiconductor tools are optimized for uptime, precision, and reliable performance, keeping your FAB competitive.

2. Automotive & EV Power

Modern vehicles (especially EVs and ADAS) pack 2–3× more chips than gasoline cars[4]. Much of this is power electronics and sensors, roughly 30–40% of auto semis are wide-bandgap power devices[4]. Fabricating SiC or GaN devices requires specialised deposition (e.g. thick epitaxial oxides) and etching tools tailored to hard materials. Advanced driver-assist also uses mmWave radar ICs, demanding sub-100 GHz RF design techniques on silicon.

Our Process Engineering expertise helps FABs optimise their process and efficiency by fine-tuning critical steps for advanced automotive and power devices.

3. Sensors & MEMS

Image sensors, accelerometers, gyros, and other MEMS/NEMS devices proliferate in phones, cars, and IoT nodes. These require deep silicon etch (often “Bosch” DRIE processes) and wafer-scale packaging. Even “conventional” CMOS chips now embed MEMS and analogue sensors (capacitive touch, pressure, IR, etc.).

As one report notes, IoT devices blend analogue-to-digital circuitry, RF chips, power modules and sensors to “sense the analogue world”[1], imposing new process integration challenges. With our FAB Facility Services, we help FABs maintain world-class cleanroom environments and infrastructure to support complex MEMS and sensor manufacturing.

Combined, ICAPS semiconductor market trends are propelling equipment innovation. As an instance, fabs are repurposing 300mm assets to economically run mature nodes for IoT/auto chips[2], and developing new materials (high-k dielectrics, metal gates, SiC epitaxy) to achieve power/sensor specs. The challenge for semiconductor equipment innovation, therefore, is to enable multi-dimensional innovation going beyond transistor scaling to incorporate new materials, architectures and integration strategies[1].

Semiconductor Trends and RF Technologies in RF Circuit Design

1. RF Circuit Design Fundamentals in ICAPS Applications

Radiofrequency (RF) circuit design is central to ICAPS applications. RF design involves creating systems and components (amplifiers, filters, mixers, antennas) that operate at high frequencies[5].

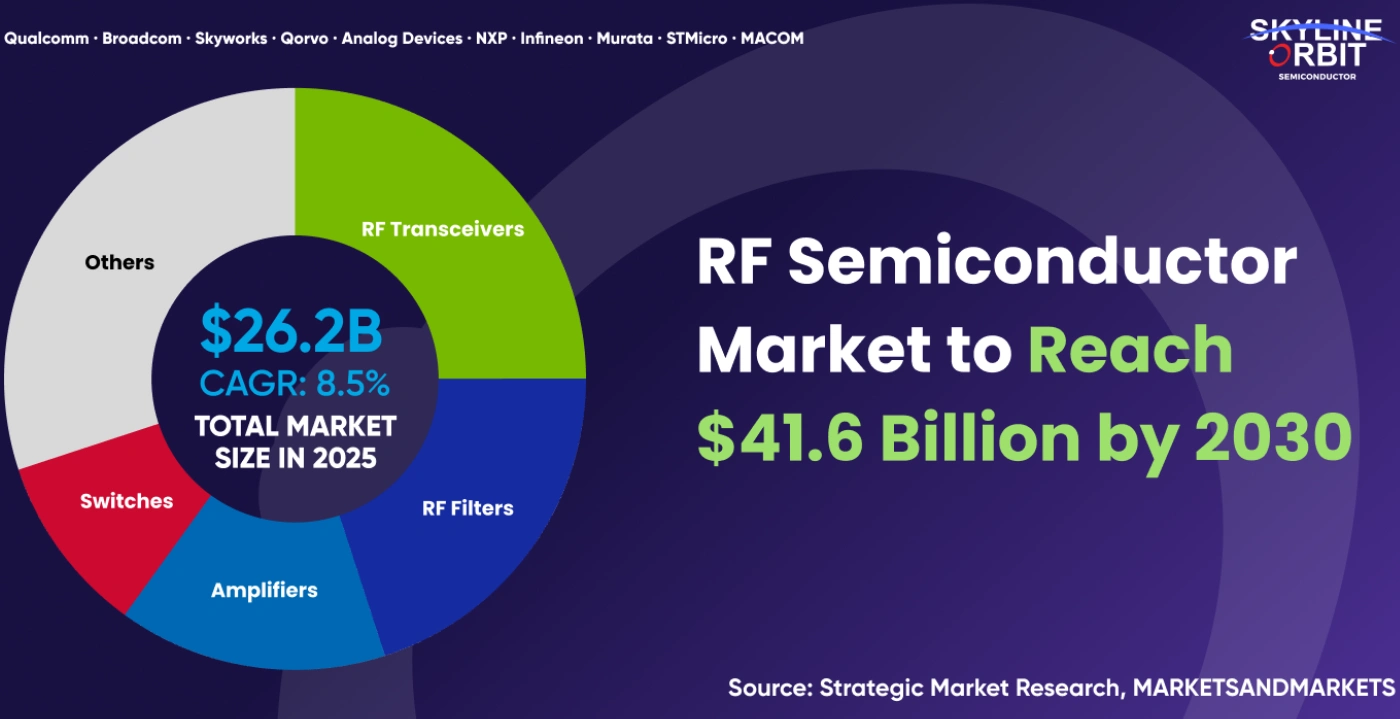

In practice, this means integrating complex front ends (e.g. 5G transceivers, Bluetooth radios, radar PAs) on silicon or compound substrates. The RF technologies in semiconductor fabrication reflect this growth projected from $25.7 B in 2024 to $41.6 B by 2030, powered by 5G rollouts, IoT connectivity and automotive radar[3]. For instance, global RF chip forecasts highlight 5G, satellite comms and vehicle radar as key drivers, making RF components “increasingly indispensable” in both consumer and industrial devices[3].

2. Advanced RF SoC Design for IoT and Automotive

Connecting billions of devices requires advanced RF SoC design. Low-noise amplifiers, phase shifters, and antenna tuners must be co-designed with digital logic. To keep battery life long, many IoT RF chips leverage analogue/mixed-signal tweaks on mature nodes (e.g. 28–55 nm).

Indeed, to meet IoT demands, “RF-optimised versions” of standard processes (28/22/16 nm) are being developed, enabling lower-power BLE and LoRa radios[1]. In automotive, Radio Frequency expertise is key for radar/LiDAR: silicon, GaAs or SiGe processes are used to achieve the necessary frequency and linearity.

3. Impact of RF Design on Semiconductor Equipment Requirements

It also depends on the Radio Frequency (RF) design techniques and equipment needs. High-frequency analogue often needs different BEOL (back-end-of-line) materials, notably low-loss dielectrics and thick copper; this drives equipment vendors to support new tool recipes (for example, deep trench isolation steps or additional metal layers).

In parallel, the breathtaking volume of RF IoT chips requires high-throughput etch/deposition tools. RF circuits have characteristics beyond chip-level design rules and not just for systems IC development; they are also shaping semiconductor equipment innovation[1].

Semiconductor Trends and RF Technologies in Plasma-Based Fabrication Processes

Many critical semiconductor fabrication steps rely directly on RF energy. In etching and deposition, RF-powered plasmas enable fine control at the nanoscale. For example, semiconductor chambers use a plasma (ionised gas) to etch or deposit films, with RF generators supplying the energy.

As one review explains, inside a process chamber, “partially ionised gas, called plasma, is used to accomplish deposition, etching, and cleaning”, and “the generation and sustaining of a plasma is possible with RF energy”[6].

In practice, RF sources (often 13.56 MHz or 27.12 MHz) are coupled into a chamber through a matching network, energising gas molecules so they react with the wafer surface. The level and purity of this RF power critically affect uniformity and selectivity: “RF energy applied carries great importance to accomplish selective wafer processing, including uniformity, etch rate, and anisotropy”[6].

Key Radio Frequency (RF) Driven Processes in Semiconductor Fabrication

Key RF-driven processes include:

1. Atomic Layer Deposition (ALD)

An ultra-precise CVD method that deposits films one atomic layer at a time. ALD’s self-limiting pulses yield conformal, ultra-thin coatings (e.g. gate oxides, high-κ dielectrics) critical for nanoscale devices[7]. ALD chambers often use plasma (RF bias) steps to clean surfaces between pulses.

2. Plasma-Enhanced CVD (PECVD)

Uses an RF-powered plasma to activate film deposition at lower temperatures. For example, PECVD silicon dioxide or nitride films are formed by dissociating silane/other precursors with RF energy[7]. This enables high-quality insulators on temperature-sensitive substrates.

3. Reactive Ion Etching (RIE)

A dry etch combining chemical reactions and ion bombardment under RF plasma. RIE “uses reactive gases in a plasma state to chemically and physically remove material” with high resolution and anisotropy[8]. The RF bias accelerates ions vertically, producing directional (anisotropic) etch profiles – essential for tight patterning. As one technical guide notes, RIE’s ion bombardment yields sharp, well-defined features with minimal undercutting. In practice, many RIE systems operate at 13.56 MHz RF[8].

4. Inductively Coupled Plasma (ICP) Etch

Uses an RF coil to inductively couple energy into the chamber, creating a high-density plasma. ICP tools (often combined with RIE bias) are used for deep or high-aspect-ratio etches, such as MEMS trenches or through-silicon vias. These rely on RF power both in the coil and the substrate bias[8].

5. Physical Vapor Deposition (PVD)

Sputtering processes for metal or dielectric layers. While many PVD systems use DC for conductive targets, sputtering insulators (like silicon oxide) may use RF power. RF sputtering sources are a variant of RF power delivering ions to knock material onto the wafer[7].

In all these tools, RF generators and matching networks are critical subsystems[6]. The RF frequency and power level determine ion energy and density, affecting etch rate and film quality. For instance, high RF bias enhances anisotropy in RIE, while high-density RF plasma (e.g. 2–4 MHz in ICP) boosts etch throughput.

Equipment engineers must therefore design RF delivery for low noise and stable impedance, since “spurious and harmonics levels” must be tightly controlled in chip fabrication[6]. RF energy remains a core enabler of modern wafer fabrication, from atomic-layer deposition to sub-20 nm anisotropic etching.[8].

Semiconductor Trends and RF Technologies in India’s Semiconductor Expansion

1.Government Initiatives and Policy Support

Globally, governments are accelerating semiconductor capacity expansion, and Semiconductor manufacturing in India is positioning itself as an emerging hub. The government’s $10 billion India Semiconductor Mission aims to establish local chip fabs, package/test facilities and R&D[9].

Under this program and initiatives like “Make in India”, incentives are offered to attract international manufacturers and develop domestic start-ups[9]. Progress includes funding new wafer fabs and packaging units, with a long-term goal to reduce reliance on imports.

2. 5G, EV Growth and ICAPS Market Drivers

India’s semiconductor strategy aligns with its domestic electronics demand, digital infrastructure expansion, and EV growth trajectory. Analysts highlight the rollout of 5G networks (by carriers like Jio/Airtel) and a booming EV sector as key market drivers[9]. For example, the growth of India’s EV semiconductor demand (and worldwide) sharply increases demand for automotive semis (sensors, controllers, power ICs)[4].

Similarly, smart city and Internet of Things (IoT) initiatives (in healthcare, agriculture, and energy) fuel specialised chips. India-Briefing notes that 5G/telecom, automotive/EV and IoT are “key trends shaping India’s semiconductor market growth,” each spurring demand for high-performance chips[9].

India is hoping its electronics market (for exhibits like smartphones and IoT devices) will be worth hundreds of billions of dollars in many years and might want a strong supply chain.

Through the combination of advanced engineering solutions along with strategic product oversight, our Engineering & Product Management Services help semiconductor manufacturers optimise costs, drive product reliability, and mitigate time-to-market.

3. Equipment Demand and Future Outlook

In conclusion, the semiconductor ecosystem in India is likely to see significant opportunities in terms of volumes and innovations, backed by policy incentives and a large electronics manufacturing base. As a result, as semiconductor manufacturing in India takes hold and expands, Semiconductor FABs and design houses will turn to the advanced equipment for ICAPS technologies (e.g. tools for RF front ends, MEMS sensors, power devices) that are necessary for cutting-edge fabrication.

Distributor partnerships and research centers are also helping bridge global semiconductor knowledge into India’s market. While challenges remain (building human expertise, supply chain), the combination of policy support and market growth means India will increasingly be part of the global chipmaking story[9].

Conclusion: RF Technologies Shaping the ICAPS Era

Thus, in short and simple terms, the ICAPS wave is changing the FAB floor. New chip architectures and materials are now dominated by IoT, comms, auto, power and sensor end-markets with RF technologies at the nexus of these changes. Authors[4] wrote about RF circuit design with the ability to empower connectivity and sensing on chip, while others[5] focused on the use of RF-powered plasmas to achieve precise etching and depositing next-gen devices. For equipment engineers and process experts, the future is about innovating RF delivery, plasma control and materials integration to meet demand in this diverse, high-engagement semiconductor landscape.

With 15+ years of expertise and a global team of 500+ engineers, Orbit & Skyline is a trusted partner in the semiconductor industry. If you are looking for a semiconductor services and solution partner, reach out to us at hello@orbitskyline.com.

References

Recent industry analyses and technical reviews on ICAPS markets, RF semiconductor growth[1], RF circuit design[5], plasma and deposition processes[8], and India’s semiconductor initiatives[9].

- [1] What’s Driving the Need for Innovation in ICAPS? https://www.appliedmaterials.com/us/en/newsroom/perspectives/whats-driving-the-need-for-innovation-in-icaps.html

- [2] Leveraging 300 mm Technologies at 200 mm for IoT and Automotivehttps://newsroom.lamresearch.com/Leveraging-300-mm-Technologies-at-200-mm-for-IoT-and-Automotive

- [3] RF Semiconductor Market Size ($41.6Billion) 2030https://www.strategicmarketresearch.com/market-report/rf-semiconductor-market

- [4] Automotive Semiconductor Demand: How EVs Are Driving Chip Market Growth | PatentPC https://patentpc.com/blog/automotive-semiconductor-demand-how-evs-are-driving-chip-market-growth

- [5] RF Design Software Market, Report Size, Worth, Revenue, Growth, Industry Value, Share 2024https://reports.valuates.com/market-reports/QYRE-Auto-37P18173/global-rf-design-software

- [6] Mwjournalmwj201312 DL | PDF | Telecommunications | Telecommunications Engineeringhttps://www.scribd.com/document/200069881/Mwjournalmwj201312-Dl

- [7] The Role of Plasma Technology and Deposition Techniques in Semiconductor Manufacturing – RFHIChttps://rfhic.com/industries-rf-energy/industrial/the-role-of-plasma-technology-and-deposition-techniques-in-semiconductor-manufacturing/

- [8] Reactive Ion Etching: A Comprehensive Guidehttps://www.wevolver.com/article/reactive-ion-etching

- [9] India’s Emerging Semiconductor Ecosystem: Key Players

https://www.india-briefing.com/news/india-emerging-semiconductor-ecosystem-key-players-34506.html

Semiconductor FAB Solutions

Semiconductor FAB Solutions

OEM Solutions

OEM Solutions